Truman-Nock House

The Truman-Nock House from "Beautiful Pewee Valley," published by Powhatan Wooldridge and George Washburne in 1909. Photo reproduction from "Pewee Valley: Land of the Little Colonel" published by Katie S. Smith in 1974. The photo first appeared in the April 4, 1897 Courier-Journal in an article titled, "Some of the Pretty Homes of Pewee Valley." At that time it was owned by W.N. Jurey.

The oldest house on the south side of Pewee Valley’s Ash Avenue Historic District is the Truman-Nock house at 116 Ash Avenue. The National Register nomination notes that the two-story Queen Anne was probably built about 1890 by H.C. Truman to replace an earlier house that burned. His biography, however, shows that the Trumans were living in Pewee Valley as early as 1888, probably with Harry's widowed mother at another National Register property now known as the Truman-Miller-Richard House.

The Truman Years

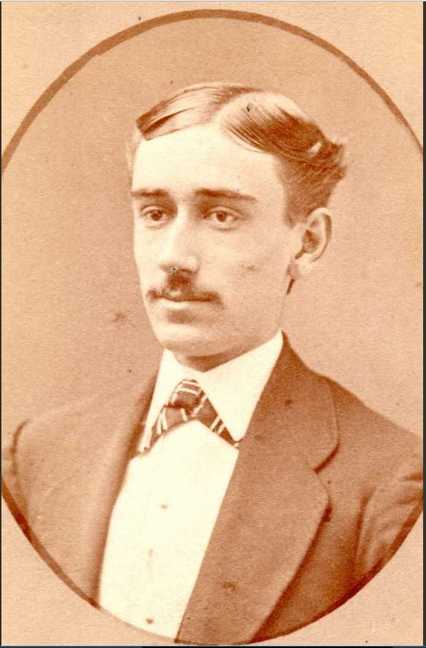

Harry C. Truman (August 4, 1850-September 21, 1904). From ancestry.com.

Harry C. Truman (August 4, 1850-September 21, 1904). From ancestry.com.

A biography of Harry C. “H.C.” Truman, written by his wife, Hattie Semple, was published in “Kentucky: A History of the State,” by Perrin, Battle, Kniffin, 8th ed. (Jefferson Co.; 1888):

HARRY C. TRUMAN, cashier of the Kentucky National Bank, was born in this city, August 4, 1850, and is a son of Orville and Esther (Marriner) Truman, the former for many years a leading wholesale merchant, and the latter one of the leading hardware merchants of Louisville. The subject of the sketch was educated in the public schools of Louisville, and for a term was a student in Murray Hill Institute, New York City, and completed his educational studies in a private class of Prof. B. B. Huntoon of this city. He engaged in the banking business in 1868, first taking a position in the Bank of America of this city, which in a few years went into voluntary liquidation. He was then offered a position in the Kentucky National Bank, and has been with that bank ever since, holding different positions, and by strict business integrity has arisen to the important one of cashier. He was married in September, 1881, to Miss Hattie Semple, a daughter of A. C. Semple, of Louisville, a prominent citizen and business man. Mr. Truman lives at Pewee Valley, sixteen miles from Louisville, on the Shortline Railroad, one of the most delightful suburban retreats adjacent to Louisville.

HARRY C. TRUMAN, cashier of the Kentucky National Bank, was born in this city, August 4, 1850, and is a son of Orville and Esther (Marriner) Truman, the former for many years a leading wholesale merchant, and the latter one of the leading hardware merchants of Louisville. The subject of the sketch was educated in the public schools of Louisville, and for a term was a student in Murray Hill Institute, New York City, and completed his educational studies in a private class of Prof. B. B. Huntoon of this city. He engaged in the banking business in 1868, first taking a position in the Bank of America of this city, which in a few years went into voluntary liquidation. He was then offered a position in the Kentucky National Bank, and has been with that bank ever since, holding different positions, and by strict business integrity has arisen to the important one of cashier. He was married in September, 1881, to Miss Hattie Semple, a daughter of A. C. Semple, of Louisville, a prominent citizen and business man. Mr. Truman lives at Pewee Valley, sixteen miles from Louisville, on the Shortline Railroad, one of the most delightful suburban retreats adjacent to Louisville.

|

This profile of the Kentucky National Bank, written by Young Ewing Allison, appeared in “The City of Louisville and a Glimpse of Kentucky,” published by the Committee on industrial and commercial improvement of the Louisville board of trade in 1887:

THE largest business done by any bank in Kentucky, probably the largest south of the Ohio river, is that of the Kentucky National Bank, which, though young in years, occupies a place second to that of no other financial institution in Louisville. The bank was organized in December, 1871, the late Bland Ballard, Judge of the United States District Court, being its first President, and Mr. Logan C. Murray its first Cashier. The capital stock was originally $300,000, but a rapidly increasing business shortly demanded that the capital be raised, and it was accordingly increased to $500,000. This increase was made in 1874 and the capital stock has since remained at these figures. When the bank was founded it at once mapped out a progressive policy, though its business was conducted within the strictest rules of safe finance. Its officers then and since have sought every legitimate opportunity to acquire business through every proper channel, going somewhat out of the beaten paths of less energetic banks located in the interior of this country. Judge Ballard remained the President of the bank until his death, which occurred on July 29, 1879. Mr. Logan C. Murray succeeded him and retained the Presidency until March, 1881, when he resigned and went to New York, where, with Mr. H. Victor Newcomb, he founded the United States National Bank, of which he is now the President. Upon Mr. Murray's election to the Presidency of the Kentucky National Bank Mr. James M. Fetter, who had been the Teller, was made Cashier, and when Mr. Murray resigned the Presidency, the management of the affairs of the institution fell entirely into the hands of the Cashier, the post of President becoming little more than an honorary one, until Mr. Fetter was himself elected President in 1885. The bank makes special features of collections at home and abroad, the purchase and sale of government bonds and sterling exchange, and issues letters of credit to all foreign countries. It is, in fact, the headquarters in Louisville for all foreign business. The immense purchases of tobacco made in this market by foreign buyers being the chief basis of this branch of its business. The bank keeps its London account with the Union Bank of London, Limited. It also does the largest interior business south of the Ohio river, and its mail is said to be the largest received by any corporation in Louisville except the newspapers. The bank's statement in October, 1872, shows a total footing of $737.612.56, with deposits of $174,147.28. On October, 1877, the business had increased so that the deposits amounted to $858.229.60, the statement on that date showing a total footing of about $2,000,000. The last statement on August 1, 1887, is as follows: |

Hattie Semple Truman (1859-December 1, 1935), Harry's wife, with their son, Harry C. Truman, Jr. From ancestry.com.

Harry C. Truman later in life. From ancestry.com.

|

The bank is centrally located at Fifth and Main streets, and occupies handsome offices. It was the first of the Louisville banks to fit up its establishment with elegance and taste, and it is worthy of remark that nearly every bank in the city has followed its example, though none of them have surpassed the Kentucky National either in the appearance of their interiors or the convenience of their arrangements and appliances.

The officers of the Kentucky National Bank are James M. Fetter, President; A. M. Quarrier, Vice-President; H.C. Truman, Cashier. The Directors are Julius Winter, A. M. Quarrier, W. H. Thomas, A. C. Semple, W. H. Coen, W. W. Hite, J. B. Owsley, J. S. Grimes, and James M. Fetter. It has been under Mr. Fetter's management that the bank has reached its greatest prosperity. He is one of the foremost men in the commercial world of the South and South-west, and is doing much for the development of Lousiville and of Kentucky. Mr. Fetter is a native of Jefferson county and is now only forty years of age. He was at college at Georgetown, D. C., when he was appointed a cadet in the military academy at West Point, where he remained until the breaking out of the war, when he, like other Southern boys, returned to his home. After some mercantile experience he became a clerk in the Falls City Bank, but left this position upon the organization of the Kentucky National Bank. He rose step by step until he was made Cashier, having won the confidence of the officers of the bank. Having for some time been the practical head of the institution, on January 1, 1881, he was elected its President, thus becoming also the nominal head. He is a Director in the Louisville, New Albany & Chicago Railroad, the Louisville, Evansville & St. Louis Railroad, and in some eight or ten other important corporations. Mr. Fetter is a man of the most perfect polish of manner, of the soundest judgment, and the quickest perceptions. When he acts boldly, he acts upon a conviction that amounts to a certainty. Mr. Truman, the Cashier, is also a young man. He entered the bank as correspondent clerk in 1872, was made Assistant Cashier when Mr. Fetter was elected Cashier, and was promoted to Cashier in 1885, and, having had experience in every department in banking, is a thoroughly equipped officer. To his systematic care and progressive policy in the management of the office work is due much of the growth and popularity of the bank.

Harry’s parents, Orville and Esther Truman, also lived in Pewee Valley at what is now known as the Truman-Miller-Richard house. By the time he built his Ashwood Avenue home, however, his father, who was an original town trustee when Pewee Valley was incorporated in 1870, had been dead for many years.

Harry and Hattie had six children:

The family lived in Pewee Valley only seven years. The 1900 census lists Harry as a patient at the Central State Lunatic Asylum, where he died in 1904 from what appear to be medical complications of a mental disorder. His family had by then moved back to Louisville.

Harry and Hattie had six children:

- Lillian S. Truman (January 1882- November 6, 1962); she never married and worked as a housemother

- Orville Truman (September 12, 1884-May 29, 1971); he was married to Artina Truman and never had children.

- Frances Truman (August 1886-?)

- Harry Clarence Truman, Jr. (January 27, 1890-March 1978). He was married to Mariah Louise Cunning and had one daughter.

- Alix S. Truman (May 1895-?)

- Esther Truman (September 1896-?)

The family lived in Pewee Valley only seven years. The 1900 census lists Harry as a patient at the Central State Lunatic Asylum, where he died in 1904 from what appear to be medical complications of a mental disorder. His family had by then moved back to Louisville.

Truman Family Graves at Cave Hill Cemetery

The Truman-Nock house. Photo from "Historic Pewee Valley," published by Historic Pewee Valley, Inc. in 1991.

The Nock Years

|

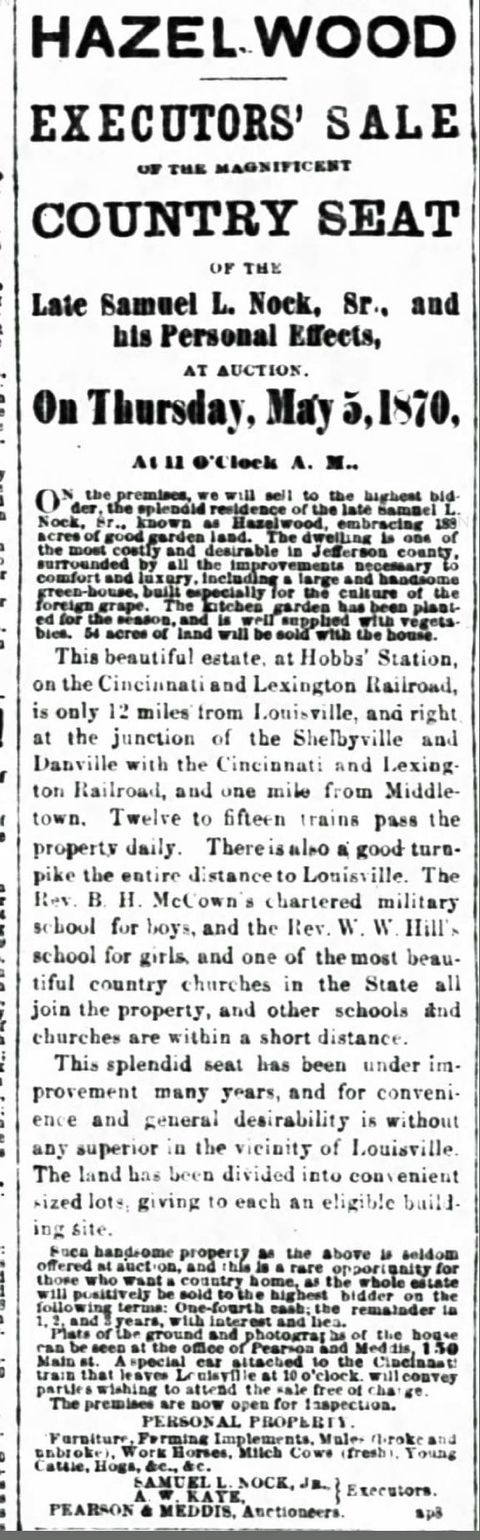

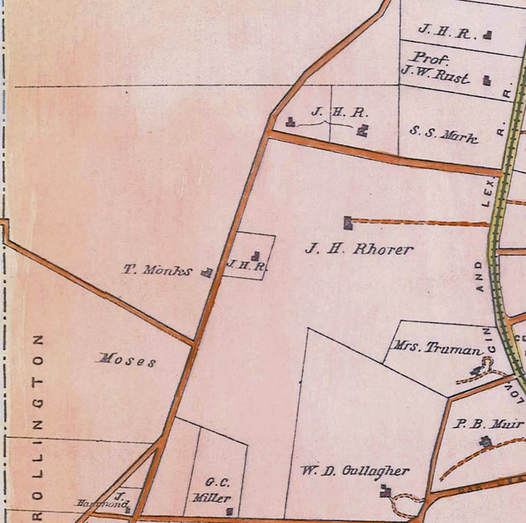

In 1897, the house was purchased by Robert Fulton Nock (1844-September 6, 1933) and Annie Courtney Monks Nock (December 2, 1853-September 13, 1929). Robert was a practicing attorney. According to the 1894 “Catalogue of the Phi Delta Theta Fraternity,” he graduated with an A.B. from St. Francis Xavier in 1864 and an L.L.B. from Harvard in 1866. Trowe’s Legal Directory and Lawyers’ Record of the United States, written by H. Charles Ulman (John F. Trowe; 1875) listed him with the firm of Munday & Parsons in Louisville. Other lawyers at Munday & Parsons included Louis Nahm, L. Noble, II, John W. Owings, L.L. Parks, W.C. Pegram and H.C. Pindell. Robert was the son of Samuel L. Nock (December 29, 1804-January 24, 1867) and Jane Lawless Beckwith Nock (June 5, 1902-July 12, 1893) and had spent part of his childhood in neighboring Anchorage, where his parents owned an estate known as Hazelwood. According to an obituary for his brother, Samuel, Jr., that ran in the October 29, 1905 Courier-Journal: ... Samuel L. Nock was a member of the firm of Nock & Rawson before the war, the largest tobacco and wholesale grocery concern in Louisville. A picture of their store was found in the corner-stone of the old Masonic Temple when it was demolished a week ago. Mr. Nock's grandfather was George B. Nock, one of the pioneers of Louisville, who came here in 1817 and established a foundry on the site of the City Hall... Robert's sister, Virginia Nock Kaye, had also lived in Pewee Valley for a time. She and her husband, Dr. A.W. Kaye, owned the property once associated with the Pewee Valley Hospital & Sanitarium, where Friendship Manor is located today. Dr. Kaye, along with Robert's older brother, Samuel, Jr., served as executors of Samuel, Sr.'s large estate in Anchorage in 1870. By the time Robert and Annie moved to Pewee, both Virginia and A.W. were dead; however, their oldest son, Arthur, still owned the Kaye family farm. The Nocks also had another relation residing in Pewee Valley: Thomas Harris Monks, Annie’s brother, who was farming 30 acres on the north side of the Louisville - Brownsboro Pike (now Hwy. 22) across from The Locust’s property, according to the 1879 Beers & Langan Atlas of Pewee Valley. A profile of Thomas was included in Battle, Perrin & Kniffin’s sixth edition of “Kentucky: A History of the State,” published in 1887: THOMAS H. MONKS was born in Louisville October 8, 1837… He was educated at Drennon Military School, Henry County, and Auburndale College, Boston, Mass, acquiring, in addition to a good English education, a knowledge of Latin and French. He married, October 15, 1867, Lou Moses, daughter of William and Amanda W. Moses, of Louisville. Two sons and three daughters were born to their union. Mr. Monks owns thirty acres eleven miles from Louisville. Politically he is a Democrat. He is engaged in farming in Oldham County, near Pewee Valley. Thomas died and was buried in Cave Hill Cemetery in 1903. Thomas and Annie were the children of Joseph Monks, a prominent Louisville businessman, according “The Biographical Encyclopædia of Kentucky of the Dead and Living Men of the Nineteenth Century, Volume 1,” written by J.M. Armstrong in 1878: MONKS, JOSEPH, Merchant, was born in Bolton, Lancastershire, England, February .14, 1811. He received a liberal English education, which was finished after his removal to this country, with his parents, at Lexington, Kentucky. His father conducted the business of manufacturing bagging and rope, in that city, which was the center of a large hemp district. He was employed with his father in this business, in Lexington, Louisville, and afterwards in Hancock County, on the river, until the death of this parent, in 1831. After this event, he went to Louisville, and engaged in the liquor business, as a member of the firm of E. Talmage & Co., until 1840, when it was conducted under his name alone. For a short time, Mr. W. H. Walker was his partner, and then, for a‘space of five or six years, he carried on again for himself, his store being on Main Street, between Fifth and Sixth, and afterwards, between Sixth and Seventh Streets. In 1848, he took A. Zanone into a partnership, which, after a lapse of five or six years, was dissolved. About 1859, he admitted his son-in-law, Mr. Charles Cobb, into a share in the concern, which continued until 1872, when Mr. Cobb entered into a partnership with Mr. Muldoon, the sculptor. About this time, Mr. Monks desired to retire from active business life, and allowed his trade to decrease gradually, spending his time, since, in quietly settling up the affairs of the establishment. He has led an active business life, and, for the last two or three years, has been President of the Mutual Insurance Company, of Louisville. During 1844-5, he was a member of the City Council, and has been a Director of the Jefferson Savings Institute, Franklin Bank, First National Bank of Kentucky, and the Louisville Mutual Insurance Company—of the latter, for a space of twenty years. In 1835, he was married to a Miss Harriet Rees, daughter of James Rees, of Cincinnati, and they have had seven children, four of whom, Ellen, the wife of Charles Cobb, of the firm of Muldoon, Walton &: Cobb; Annie, wife of Robert F. Nock, a lawyer of Louisville; Thomas H., a farmer of Pewee Valley; and Charles H., of Louisville, still survive. Mr. Monks is a fine-looking old gentleman, with the air of contentment about him; his life and business characteristics are those of the old English style, slow and sure. He is |

Above, 1977 photo of the Hazelwood estate in Anchorage, Ky., built by Robert Fulton Nock's parents, Samuel L. and Jane Lawless Beckwith Nock ca. 1858. The house later became known as Gray Tower and was popular with summer boarders. From the National Register of Historic Places.

.

May 3, 1870 Courier-Journal

Arthur Kaye home in Pewee Valley in 1974. From "Pewee Valley: Land of the Little Colonel" published in 1974 bt Katie S. Smith.

Thomas H. Monks estate in Pewee Valley, from the 1879 Beers & Lanagan Atlas. The J.H. Rhorer property across from Monks' farm is called The Locust.

|

very modest in his demeanor, and possesses a temper that is not easily ruffled. His integrity and correctness are a matter of record in the business annals of Louisville, in which city he still continues to reside, a useful and respected citizen.

Joseph Monks died on March 19, 1889 in St. Louis. His obituary ran in the Courier-Journal the following day:

JOSEPH MONKS DEAD

________

The Termination in St. Louis of a Busy and Honorable Business Life

________

Arrangements Made For the Funeral services At St. Paul’s Church Tomorrow

The death of another prominent and universally respected gentlemen, a former resident of Louisville, with whose interests he was identified for nearly half a century, was reported yesterday from St. Louis – that of Mr. Joseph Monks.

Mr. Monks was born in England February 14 1811, but came to the United States in 1818, to Baltimore where he remained for some time. From Baltimore he moved to Lexington, Ky., where he resided until 183-, when he took up his residence in Louisville. After being a resident of this city for a time, he embarked in the whisky business, in which he continued for many years, a portion of the time under his own name and later under the style of J. Monks & Cobb. He was elected a director of the Kentucky and Louisville Insurance Company December 7, 1846, and President of the company January 8, 1875. He was a director at the time of his death, having served in that capacity for forty-three years. In July 1860, he resigned the presidency, and intended to leave the directory also, but was persuaded to withdraw his resignation as to the latter office. The death of his wife in that year (editor’s note: his wife appears to have died in 1881, not 1860), after a long and unusually happy married life, described by one of his friends as “a continual courtship,” affected him so deeply that he prepared to retire from all connections with business; hence his resignation from the presidency.

In addition to his interests in the Kentucky and Louisville Insurance Company, Mr. Monk was a large stockholder in the Louisville Banking Company, the New Albany Woolen Mills, was a stockholder and director in the Belknap-Dumesnil Stone Company, and possessed large property in Louisville, St. Louis and Texas. He was also a director in the First National Bank for a number of years, and in the Jefferson Savings Bank. His fortune was very large. For the past few years, he has divided his time between Louisville, St. Louis and New York.

Mr. Monks leaves two sons and two daughters, Thomas H. and Charles H. Monks, Mrs. Robert Nock of Pewee Valley and Mrs. Charles Cobb, of New York.

In his business relations he was a man of the strictest integrity, and in private character was beyond reproach. Many charitable deeds are his to his credit, which will never be known unless accidentally revealed. He was one of those men who shrink from publicity and apparently believed in not letting the right hand know what his left hand did. As remarked by one of his friends, “He was one of those men who, when detected in an act of charity, as he sometimes was, he always seemed to be ashamed of it and endeavored to create the impression that he had done nothing.” The universal testimony as to Mr. Monk’s character, public and private, is that he was one of the best men that ever made this city his home.

His body will be brought in Louisville for interment, arriving here at 7:10 o’clock this morning, over the O. and M., and will be taken to the residence of Mr. William Moses, Jefferson Terrace, Floyd street. The funeral will take place at 3 o’clock to-morrow afternoon from St. Paul’s Episcopal Church. The active pallbearers will be Messrs. James B. Cocke, James P. Marshall, William Tillman, George H. Breed, W.C. Hall, W.W. Thomson, Adolph Schmidt and Thomas Courtney. The honorary list embraces Messrs. George F. Downs, Thomas P. Jacob, John T. Moore, Thomas Sinton, James Bridgeford, William H. Granger, William Moses, John D. Taggart, George Davis, J.W. Davis, W. George Anderson and Dr. D.W. Yandell.

Joseph Monks died on March 19, 1889 in St. Louis. His obituary ran in the Courier-Journal the following day:

JOSEPH MONKS DEAD

________

The Termination in St. Louis of a Busy and Honorable Business Life

________

Arrangements Made For the Funeral services At St. Paul’s Church Tomorrow

The death of another prominent and universally respected gentlemen, a former resident of Louisville, with whose interests he was identified for nearly half a century, was reported yesterday from St. Louis – that of Mr. Joseph Monks.

Mr. Monks was born in England February 14 1811, but came to the United States in 1818, to Baltimore where he remained for some time. From Baltimore he moved to Lexington, Ky., where he resided until 183-, when he took up his residence in Louisville. After being a resident of this city for a time, he embarked in the whisky business, in which he continued for many years, a portion of the time under his own name and later under the style of J. Monks & Cobb. He was elected a director of the Kentucky and Louisville Insurance Company December 7, 1846, and President of the company January 8, 1875. He was a director at the time of his death, having served in that capacity for forty-three years. In July 1860, he resigned the presidency, and intended to leave the directory also, but was persuaded to withdraw his resignation as to the latter office. The death of his wife in that year (editor’s note: his wife appears to have died in 1881, not 1860), after a long and unusually happy married life, described by one of his friends as “a continual courtship,” affected him so deeply that he prepared to retire from all connections with business; hence his resignation from the presidency.

In addition to his interests in the Kentucky and Louisville Insurance Company, Mr. Monk was a large stockholder in the Louisville Banking Company, the New Albany Woolen Mills, was a stockholder and director in the Belknap-Dumesnil Stone Company, and possessed large property in Louisville, St. Louis and Texas. He was also a director in the First National Bank for a number of years, and in the Jefferson Savings Bank. His fortune was very large. For the past few years, he has divided his time between Louisville, St. Louis and New York.

Mr. Monks leaves two sons and two daughters, Thomas H. and Charles H. Monks, Mrs. Robert Nock of Pewee Valley and Mrs. Charles Cobb, of New York.

In his business relations he was a man of the strictest integrity, and in private character was beyond reproach. Many charitable deeds are his to his credit, which will never be known unless accidentally revealed. He was one of those men who shrink from publicity and apparently believed in not letting the right hand know what his left hand did. As remarked by one of his friends, “He was one of those men who, when detected in an act of charity, as he sometimes was, he always seemed to be ashamed of it and endeavored to create the impression that he had done nothing.” The universal testimony as to Mr. Monk’s character, public and private, is that he was one of the best men that ever made this city his home.

His body will be brought in Louisville for interment, arriving here at 7:10 o’clock this morning, over the O. and M., and will be taken to the residence of Mr. William Moses, Jefferson Terrace, Floyd street. The funeral will take place at 3 o’clock to-morrow afternoon from St. Paul’s Episcopal Church. The active pallbearers will be Messrs. James B. Cocke, James P. Marshall, William Tillman, George H. Breed, W.C. Hall, W.W. Thomson, Adolph Schmidt and Thomas Courtney. The honorary list embraces Messrs. George F. Downs, Thomas P. Jacob, John T. Moore, Thomas Sinton, James Bridgeford, William H. Granger, William Moses, John D. Taggart, George Davis, J.W. Davis, W. George Anderson and Dr. D.W. Yandell.

Nock Family Photos from ancestry.com

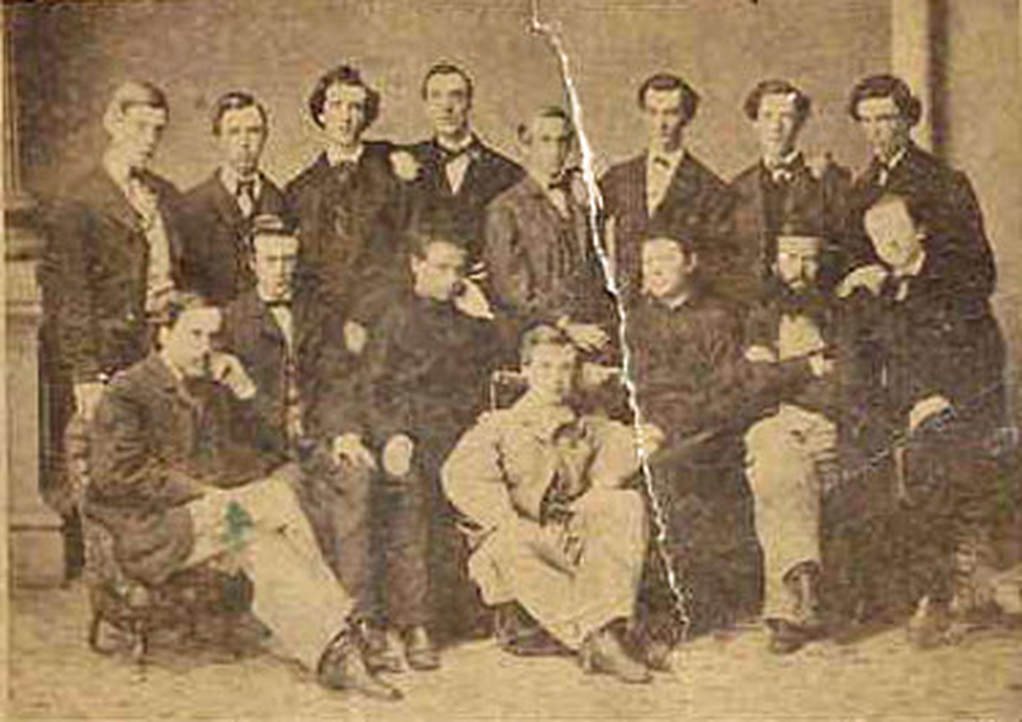

Photo showing Robert Fulton Knock, age 20, with classmates at St. Xavier College, NY, where he attended college.

Daughter Jospehine Nock, likely taken by her neighbor at Clovercroft, Kate Matthews. Josephine may have been named for her maternal grandfather, Joseph Monks. She married a Cleveland, Ohio-area man, Martin Dunbar, in 1921.

Annie and Robert Nock had six children, five of which -- Robert, Josephine, Annie, Richard and William -- were living with them in Pewee Valley at the time of the 1900 census:

- Harriett "Hallie" Nock Armstrong (August 16, 1873-April 28, 1953), who married Albert M. Armstrong in Jeffersonville, Indiana, on May 30, 1896 and returned to Pewee Valley in 1920, after being widowed.

- Robert Joseph Nock (January 22, 1876- February 1, 1968), who married Stephanie Mickle on August 29, 1913 in New Orleans, La., and remained there the rest of his life. He worked many years in the wholesale fur and hide trade and later as secretary of the Louisiana Land and Exploration Company, now one of the largest independent oil and gas exploration companies in the United States.

- Josephine Nock Farrish Dunbar (March 20, 1878-May 16, 1942), who married twice, first to Joseph Leet Farrish of St. Louis by whom she had a child, and after his death to Martin Dunbar in Cleveland, Cuyahoga County, Ohio on April 5, 1921.

- Anna C. Nock Stock (July 3, 1881-?)

- Richard Nock (1885- August 4, 1961)

- William Nock (January 12, 1887-January 15, 1958)

By the 1910 census, the Nocks' daughter, Josephine, had had a daughter, Anna Lucille "Lucy" Farrish. Her husband died in 1906, the year after Lucy was born, and both the Nocks' widowed daughter and four-year-old granddaughter were living with them in Pewee Valley. Also living at the house were Robert, Anna, Richard and William.

Scandal erupted in the Nock family in 1912, when daughter Anna ran off and eloped with a man she had met through correspondence. The January 27, 1912 Courier-Journal carried the story:

GRANDDAUGHTER OF

TOBACCO KING SEEKS MATE

_________________________________

MRS. EDWARD W. WILLIAMS

BRIDE FOR LESS THAN DAY.

________________________________

UP UNTIL WEDENSDAY NIGHT

SHE WAS MISS ANNA NOCK.

___________________________________

MARRIED IN JEFFERSONVILLE

Less than twenty-four hours after becoming a bride, Mrs. Edward W. Williams, who was Miss Anna M. Nock, daughter of Robert F. Nock, of Pewee Valley, and granddaughter of John Finzer, deceased, the millionaire tobacco manufacturer, appeared before Chief of Police Lindsey yesterday afternoon and asked the assistance of the department in locating her husband. Williams left her during the morning, she declared.

The couple were married by Magistrate Oscar J. Hay in Jeffersonville Wednesday night. To Hay they declared that they had met through correspondence while the bridegroom was a solder in the army, from which he was discharged recently. Williams asserted he was the son of Andrew B. Williams, a New York State Senator, and that his home was in Buffalo, N.Y. He gave his age as 21 years and his occupation as chauffeur.

Mrs. Williams is 27 years of age. With her sister, Miss Josephine Nock, she came to Louisville several days ago. Her mother, Mrs. R. F. Nock, declared over the phone last night that she knew nothing about her daughter's marriage until the latter called her up and told her of it. According to the mother, the girl declared she was going to Buffalo.

Although elopements among Pewee Valley's moneyed class weren't uncommon, most ended well. Couples made it up with parents and sometimes second weddings were held. Unfortunately, Anna's elopement was a complete sham. The groom was a bounder and a cad. She never went to Buffalo, and her missing husband was never found, according to this followup story in the January 29, Courier-Journal:

REPEATS STORY

___________________

Deserted Wife and Sister Visit

Police Station.

______________________

ARE TAKEN FROM WINEROOM

BEFORE NIGHT CHIEF.

______________________

NO TRACE OF MISSING HUSBAND

HAD BEEN FOUND.

______________________

PERSUADED TO GO HOME

Accompanied by the Rev. Edward C. McAllister, pastor of the Episcopalian Church of Pewee Valley, Mrs. Edward Wilson, formerly Miss Anna Nock of Pewee Valley, who appealed to the police Thursday to assist her in locating her husband, and her sister, Miss Josephine Nock, left for their homes on the 11:30 o'clock car last night. The decision to return home was reached after a conference lasting more than two hours in the office of Night Chief of Police Ridge, in which Chief Lindsey, Maj. Ridge, Rev. McAllister and several police officers figured.

The brief career of wedlock experienced by Mrs. Wilson came to a sudden termination, as it is believed Mr. Wilson will not be located. While Mrs. Wilson seemed concerned slightly over the effect her marriage will have on her mother, Mrs. Robert F. Nock, her sister was different. During the course of the conversation in Mr. Ridge's office, Miss Josephine Nock calmly lighted and smoked four cigarettes, blowing the smoke toward the ceiling with little apparent concern.

Taken from Wineroom

__________________________________________________

The girls were taken to headquarters from the wineroom of the Helmet Cafe, Sixth and Green streets, by Lt. Gardner. The entrance into the city hall of Mrs. Wilson was the fourth or fifth made there by her during the week. Her previous trips were made in an effort, she said, to obtain a warrant for the arrest of her husband of a day. According to the girl, she was deserted in a local burlesque theater by Wilson less than twenty-four hours after their marriage in Jeffersonville, late Wednesday night.

After appearing at the office of Harry C. Nehan, Clerk of the Police Court, yesterday afternoon in quest of a warrant for Wilson's arrest the girl left the building. A short time later she called Chief Lindsey over the phone and after telling him who she was she said: "I'm all to blame." According to the chief, her voice was choked by sobs. She failed to explain wherein lay her responsibility for her husband's alleged flight.

Made Dash for Liberty

________________________________________________

On her visit to Mr. Nehan's office Mrs. Wilson walked in, removed her hat and placed it on a desk. She said nothing, but rolling up her sleeves she calmly proceeded to wash her face in a washstand in the office. Then she powdered her face. Following the completion of her toilet she told her story to Mr. Nehan. He declared her conversation was such that he refused to issue a warrant.

During their visit to the office of Maj. Ridge last night, on of the girls pushed aside the Major and, dashing from the room, gave the assembled group of police officers a merry chase around the assembly room before being recaptured. From then on she submitted peacefully to the words of advice from the police and the minister.

Some argument has arisen as to the proper name of the girl's husband. Asked last night what his name was the girl declared that when she met him he told her his name was "Williams." When the marriage ceremony was about to be performed in the office of Magistrate Oscar Hay, she said he gave his name as "Wilson." It is as "Mrs. Wilson" that she has talked to the police.

Scandal erupted in the Nock family in 1912, when daughter Anna ran off and eloped with a man she had met through correspondence. The January 27, 1912 Courier-Journal carried the story:

GRANDDAUGHTER OF

TOBACCO KING SEEKS MATE

_________________________________

MRS. EDWARD W. WILLIAMS

BRIDE FOR LESS THAN DAY.

________________________________

UP UNTIL WEDENSDAY NIGHT

SHE WAS MISS ANNA NOCK.

___________________________________

MARRIED IN JEFFERSONVILLE

Less than twenty-four hours after becoming a bride, Mrs. Edward W. Williams, who was Miss Anna M. Nock, daughter of Robert F. Nock, of Pewee Valley, and granddaughter of John Finzer, deceased, the millionaire tobacco manufacturer, appeared before Chief of Police Lindsey yesterday afternoon and asked the assistance of the department in locating her husband. Williams left her during the morning, she declared.

The couple were married by Magistrate Oscar J. Hay in Jeffersonville Wednesday night. To Hay they declared that they had met through correspondence while the bridegroom was a solder in the army, from which he was discharged recently. Williams asserted he was the son of Andrew B. Williams, a New York State Senator, and that his home was in Buffalo, N.Y. He gave his age as 21 years and his occupation as chauffeur.

Mrs. Williams is 27 years of age. With her sister, Miss Josephine Nock, she came to Louisville several days ago. Her mother, Mrs. R. F. Nock, declared over the phone last night that she knew nothing about her daughter's marriage until the latter called her up and told her of it. According to the mother, the girl declared she was going to Buffalo.

Although elopements among Pewee Valley's moneyed class weren't uncommon, most ended well. Couples made it up with parents and sometimes second weddings were held. Unfortunately, Anna's elopement was a complete sham. The groom was a bounder and a cad. She never went to Buffalo, and her missing husband was never found, according to this followup story in the January 29, Courier-Journal:

REPEATS STORY

___________________

Deserted Wife and Sister Visit

Police Station.

______________________

ARE TAKEN FROM WINEROOM

BEFORE NIGHT CHIEF.

______________________

NO TRACE OF MISSING HUSBAND

HAD BEEN FOUND.

______________________

PERSUADED TO GO HOME

Accompanied by the Rev. Edward C. McAllister, pastor of the Episcopalian Church of Pewee Valley, Mrs. Edward Wilson, formerly Miss Anna Nock of Pewee Valley, who appealed to the police Thursday to assist her in locating her husband, and her sister, Miss Josephine Nock, left for their homes on the 11:30 o'clock car last night. The decision to return home was reached after a conference lasting more than two hours in the office of Night Chief of Police Ridge, in which Chief Lindsey, Maj. Ridge, Rev. McAllister and several police officers figured.

The brief career of wedlock experienced by Mrs. Wilson came to a sudden termination, as it is believed Mr. Wilson will not be located. While Mrs. Wilson seemed concerned slightly over the effect her marriage will have on her mother, Mrs. Robert F. Nock, her sister was different. During the course of the conversation in Mr. Ridge's office, Miss Josephine Nock calmly lighted and smoked four cigarettes, blowing the smoke toward the ceiling with little apparent concern.

Taken from Wineroom

__________________________________________________

The girls were taken to headquarters from the wineroom of the Helmet Cafe, Sixth and Green streets, by Lt. Gardner. The entrance into the city hall of Mrs. Wilson was the fourth or fifth made there by her during the week. Her previous trips were made in an effort, she said, to obtain a warrant for the arrest of her husband of a day. According to the girl, she was deserted in a local burlesque theater by Wilson less than twenty-four hours after their marriage in Jeffersonville, late Wednesday night.

After appearing at the office of Harry C. Nehan, Clerk of the Police Court, yesterday afternoon in quest of a warrant for Wilson's arrest the girl left the building. A short time later she called Chief Lindsey over the phone and after telling him who she was she said: "I'm all to blame." According to the chief, her voice was choked by sobs. She failed to explain wherein lay her responsibility for her husband's alleged flight.

Made Dash for Liberty

________________________________________________

On her visit to Mr. Nehan's office Mrs. Wilson walked in, removed her hat and placed it on a desk. She said nothing, but rolling up her sleeves she calmly proceeded to wash her face in a washstand in the office. Then she powdered her face. Following the completion of her toilet she told her story to Mr. Nehan. He declared her conversation was such that he refused to issue a warrant.

During their visit to the office of Maj. Ridge last night, on of the girls pushed aside the Major and, dashing from the room, gave the assembled group of police officers a merry chase around the assembly room before being recaptured. From then on she submitted peacefully to the words of advice from the police and the minister.

Some argument has arisen as to the proper name of the girl's husband. Asked last night what his name was the girl declared that when she met him he told her his name was "Williams." When the marriage ceremony was about to be performed in the office of Magistrate Oscar Hay, she said he gave his name as "Wilson." It is as "Mrs. Wilson" that she has talked to the police.

By the 1920 census, both Anna and Josephine had left Pewee Valley. In 1921, Josephine remarried, this time to Martin Dunbar, a steamfitter (plumber) in Cleveland, Ohio. What became of Anna is unknown. The Nock's oldest child, Harriett Armstrong, had moved in with them, along with her 14-year-old son, Benjamin Robert Armstrong (April 11, 1902-Oct. 18, 1948), who was working as a telephone operator. Their oldest son, Robert, was living in New Orleans by then, but Richard and William were still living in the family home on Ash Avenue. Richard was farming and William was in the painting business.

Annie Monks Nock died on September 13. 1929. She is the only member of the Nock family whose will was filed at the Oldham County Courthouse. The will is very brief and was written just a month before her death. Obviously, from its contents, the family's relationship with daughter Anna was still strained 17 years after her failed elopement. The will's sole purpose is to make sure her daughter receives her fair share of

Pewee Valley, Ky.

The Fidelity & Cal. Trust Co.

August 10, 1929

I want my daugher Annie to have a sixth part of her grandfathers Monks estate or in other words to share equally with her brothers & sisters, when a division is made of said estate.

Annie C. Nock

P.S. Also I want my fathers will carried out to the letter

Yours Truly

Annie C. Nock

I, would like my daughter Annie share kept in Trust for her, she to have the income and at her death to revert back to the Monks estate.

Annie C. Monks

Attesting to the validity of the will were her husband, Robert Nock; her son, William Nock; her daughter Anna, who was identified as Anna M. Stock, so she appears to have either married or changed her last name; and L.F. Michael, relationship unknown.

Thanks to Oldham County Clerk Julie K. Barr for providing the Pewee Valley Historical Society with a copy of Annie Monks Nock's will.

Annie Monks Nock died on September 13. 1929. She is the only member of the Nock family whose will was filed at the Oldham County Courthouse. The will is very brief and was written just a month before her death. Obviously, from its contents, the family's relationship with daughter Anna was still strained 17 years after her failed elopement. The will's sole purpose is to make sure her daughter receives her fair share of

Pewee Valley, Ky.

The Fidelity & Cal. Trust Co.

August 10, 1929

I want my daugher Annie to have a sixth part of her grandfathers Monks estate or in other words to share equally with her brothers & sisters, when a division is made of said estate.

Annie C. Nock

P.S. Also I want my fathers will carried out to the letter

Yours Truly

Annie C. Nock

I, would like my daughter Annie share kept in Trust for her, she to have the income and at her death to revert back to the Monks estate.

Annie C. Monks

Attesting to the validity of the will were her husband, Robert Nock; her son, William Nock; her daughter Anna, who was identified as Anna M. Stock, so she appears to have either married or changed her last name; and L.F. Michael, relationship unknown.

Thanks to Oldham County Clerk Julie K. Barr for providing the Pewee Valley Historical Society with a copy of Annie Monks Nock's will.

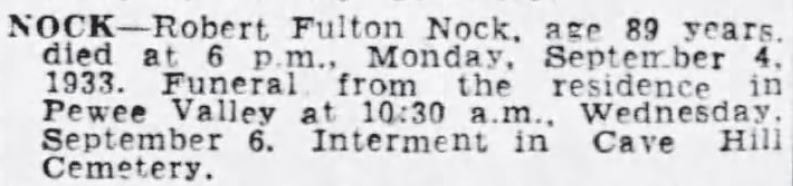

By the 1930 census, Robert was living with son Richard, who was working as a paperhanger, and daughter Harriett. He died on September 6, 1933 and his obituary ran in the Courier-Journal on September 9.

September 1974 Photos of the Truman-Nock House from the Call of the Pewee

The Nocks appear to have owned some unimproved land in Pewee Valley before they purchased their home on Ash Avenue. In December, 1896, Nock sued the City of Pewee Valley over poll taxes. A similar suit was brought by the Turners and both cases were heard together and reported in Volume 18 of “The Kentucky Law Reporter,” published by G.A. Lewis in 1897:

Turner v. Town Of Pewee Valley.

Nock v. Same.

(Filed December 10, 1896.)

These two cases, by agreement of parties, were heard together in the court below…

… They involve the same questions, and are alike in every particular except Nock seeks to enjoin the sale of his land anil collection of taxes assessed for the year 1887 by the town of Pewee Valley, in Oldham county, and Turner seeks to enjoin the sale of his land and collection assessed against him for the years 1885-6-7 by the town of Pewee Valley.

Each of appellants' lands are situated in the corporate limits of the town of Pewee Valley, and each claimed that his land is exempt from taxation because it is land used for farming land and grazing purposes, and is not benefited by reason of the corporation, and that none of said land is laid off into lots and streets; and that said land being farm land, and, therefore, they claim that their land is not subject to town taxes.

Many material questions are raised by the pleading in this record, but we consider the vital question made is the charge that the assessment of the lands of appellants for taxation is void for said town, and we deem it to be unnecessary to decide many points raised in the pleading if the court should hold that the assessment of this land for taxation was void.

The land levied on of appellants is situated within the corporate limits of the town of Pewee Valley, and was about to be advertised and sold when appellants brought these actions, and obtained an injunction enjoining said town, its trustees and the sheriff from proceeding to advertise their lands and sell the same.

The board of trustees passed an ordinance in the year 1885 by which they claim that taxes were duly levied against the lands of all citizens, and a like Ordinance was passed in the years 1886 and 1887, and the validity of the assessment made under these ordinances is the question in this case.

We quote so much of the ordinance as will be necessary to an understanding of the case: "Be it ordained by the board of trustees of the town of Pewee Valley, that an ad valorem tax of 20 cents on each one hundred dollars in value of the real estate situated in the town of Pewee Valley, Ky., liable for State taxation, be, and the same is hereby, levied. * * *

"Sec. 2. A poll tax of two dollars is hereby levied on each and every male inhabitant of said town over 21 years of age for the year 1885, for the purposes aloresaid.

"Sec. 3. For the purposes of the levy above provided the assessor is instructed to adopt the assessment list as made by the county assessor for State and county taxation for the year 1885, so far as it applies to persons and real estate within the limits of the town of Pewee Valley.

"Sec. 4. It shall be the duty of the assessor to furnish the sheriff of the county with tax bills, regularly made out, in accordance with the provision of the ordinance, on or before the 1st day of August, 1885.

"Sec. 5. The taxes levied and assessed, as aforesaid, shall be due and payable on and after August 10, 1885."

Under and by virtue of this ordinance the tax bills were levied on appellants' land, and an attempt to sell the same was made when enjoined. The ordinances made in 1880 and 1887 are an exact copy of the one made in 1885.

It is in proof, and not denied in the pleading, that the only assessment of appellants' property was made by taking a copy of the assessment made by the assessor of Oldham county for the years complained of, which list was given to the sheriff of Oldham county for collection, and the sheriff, with that authority alone, levied on the land of each appellant, and each has enjoined the town and its then trustees and the sheriff from selling their land.

We are compelled to hold that the pretended assessment of appellants' property in the mode and manner shown in these cases is void. Every tax is an involuntary charge on the taxpayer, although in some instances a community may desire and vote a tax on themselves, yet there are always some who object to being taxed, and as to those who do object it must be an involuntary charge.

The imposition of such involuntary charges of taxes on citizens is the exercise of sovereign power, and so closely is the exercise of that power guarded by constitutional provisions and by the adjudication of the courts that require a strict observance of the law under which such taxes are to be imposed. As said by Judge Cooley on Taxation: "The assessment being so important, provision respecting its preparation and contents ought to be observed with particularity. * * * The assessment must, therefore, be made by the proper officer or it will be void. * * * So the assessment will be void if the assessor commits the office of making it to a clerk." (Cooley on Taxation, pages 363-4.)

The board of trustees, by requiring the assessor of the town to adopt the assessment made by the assessor of Oldham county, not only prevented him from making an assessment himself, but required the assessor to procure an assessment made by one who was not a citizen of the town, and one who had no common interest with those who were expected to pay the tax. They failed to require even a report to the board for its approval, but directed the assessor to make out the list and give it to the sheriff for collection by these ordinances. No provision was made for the taxpayer to be heard, nor was he given any notice or opportunity to be heard and correct said list.

This question is not new to this court. Similar questions were decided in the case of Slaughter v. City of Louisville, 89 Ky., 112; Davidson v. Sterrett, 13 Ky. Law Rep., 176.

But after these suits were instituted the appellees, in the year 1890, procured an act of the Kentucky legislature, seeking to cure the defects in the assessment complained of, but this court has repeatedly held that no legislature can affect the rights of parties litigant enacted after the institution of the suits, therefore, the curative act of the legislature, attempting to affect the parties to these suits, must be treated as a nullity so far as it relates to the rights of appellants at the time of bringing their suits. (Allison v. Railway Co., 9 Bush, 247.)

But the appellees contend that the injunction ought not to have been granted because each of the appellants were charged with poll tax of $2 against appellant Nock and $6 against appellant Turner, and that the assessment of the poll tax was in form and valid.

We can not concur in this contention, although the assessment of poll tax against appellants may have been all right and legal, but still that would not authorize the sheriff to levy on appellant's land; for by the General Statutes, which was in force at the time, the sheriff had no right to levy on land and sell it for taxes until the personal property of the taxpayer had been exhausted.

The proof in these cases show clearly that appellants had an abundance of personal property within the corporate limits of the town to satisfy these taxes against them. (General Statutes, chapter 92.)

The judgment is, therefore, reversed and cause remanded, with directions that the court perpetuate the injunction in each of said cases and for further proceedings in accordance with this opinion.

The court delivered the following extension of opinion January 15, 1897:

Appellees having petitioned for an extension of the opinion heretofore filed in this case, and for further opinion, we hold that the levy or assessment of poll tax against the appellants was legal and valid, and the appellants are liable to the payment of the same, and as held in the opinion their lands were not liable to sale for the payment of the poll tax until their personal property was exhausted, and all that was intended in the former judgment was to perpetuate the injunction as to the collection of the ad valorem taxes levied, and the sale of their lands for the poll taxes, and the petition is overruled.

Turner v. Town Of Pewee Valley.

Nock v. Same.

(Filed December 10, 1896.)

These two cases, by agreement of parties, were heard together in the court below…

… They involve the same questions, and are alike in every particular except Nock seeks to enjoin the sale of his land anil collection of taxes assessed for the year 1887 by the town of Pewee Valley, in Oldham county, and Turner seeks to enjoin the sale of his land and collection assessed against him for the years 1885-6-7 by the town of Pewee Valley.

Each of appellants' lands are situated in the corporate limits of the town of Pewee Valley, and each claimed that his land is exempt from taxation because it is land used for farming land and grazing purposes, and is not benefited by reason of the corporation, and that none of said land is laid off into lots and streets; and that said land being farm land, and, therefore, they claim that their land is not subject to town taxes.

Many material questions are raised by the pleading in this record, but we consider the vital question made is the charge that the assessment of the lands of appellants for taxation is void for said town, and we deem it to be unnecessary to decide many points raised in the pleading if the court should hold that the assessment of this land for taxation was void.

The land levied on of appellants is situated within the corporate limits of the town of Pewee Valley, and was about to be advertised and sold when appellants brought these actions, and obtained an injunction enjoining said town, its trustees and the sheriff from proceeding to advertise their lands and sell the same.

The board of trustees passed an ordinance in the year 1885 by which they claim that taxes were duly levied against the lands of all citizens, and a like Ordinance was passed in the years 1886 and 1887, and the validity of the assessment made under these ordinances is the question in this case.

We quote so much of the ordinance as will be necessary to an understanding of the case: "Be it ordained by the board of trustees of the town of Pewee Valley, that an ad valorem tax of 20 cents on each one hundred dollars in value of the real estate situated in the town of Pewee Valley, Ky., liable for State taxation, be, and the same is hereby, levied. * * *

"Sec. 2. A poll tax of two dollars is hereby levied on each and every male inhabitant of said town over 21 years of age for the year 1885, for the purposes aloresaid.

"Sec. 3. For the purposes of the levy above provided the assessor is instructed to adopt the assessment list as made by the county assessor for State and county taxation for the year 1885, so far as it applies to persons and real estate within the limits of the town of Pewee Valley.

"Sec. 4. It shall be the duty of the assessor to furnish the sheriff of the county with tax bills, regularly made out, in accordance with the provision of the ordinance, on or before the 1st day of August, 1885.

"Sec. 5. The taxes levied and assessed, as aforesaid, shall be due and payable on and after August 10, 1885."

Under and by virtue of this ordinance the tax bills were levied on appellants' land, and an attempt to sell the same was made when enjoined. The ordinances made in 1880 and 1887 are an exact copy of the one made in 1885.

It is in proof, and not denied in the pleading, that the only assessment of appellants' property was made by taking a copy of the assessment made by the assessor of Oldham county for the years complained of, which list was given to the sheriff of Oldham county for collection, and the sheriff, with that authority alone, levied on the land of each appellant, and each has enjoined the town and its then trustees and the sheriff from selling their land.

We are compelled to hold that the pretended assessment of appellants' property in the mode and manner shown in these cases is void. Every tax is an involuntary charge on the taxpayer, although in some instances a community may desire and vote a tax on themselves, yet there are always some who object to being taxed, and as to those who do object it must be an involuntary charge.

The imposition of such involuntary charges of taxes on citizens is the exercise of sovereign power, and so closely is the exercise of that power guarded by constitutional provisions and by the adjudication of the courts that require a strict observance of the law under which such taxes are to be imposed. As said by Judge Cooley on Taxation: "The assessment being so important, provision respecting its preparation and contents ought to be observed with particularity. * * * The assessment must, therefore, be made by the proper officer or it will be void. * * * So the assessment will be void if the assessor commits the office of making it to a clerk." (Cooley on Taxation, pages 363-4.)

The board of trustees, by requiring the assessor of the town to adopt the assessment made by the assessor of Oldham county, not only prevented him from making an assessment himself, but required the assessor to procure an assessment made by one who was not a citizen of the town, and one who had no common interest with those who were expected to pay the tax. They failed to require even a report to the board for its approval, but directed the assessor to make out the list and give it to the sheriff for collection by these ordinances. No provision was made for the taxpayer to be heard, nor was he given any notice or opportunity to be heard and correct said list.

This question is not new to this court. Similar questions were decided in the case of Slaughter v. City of Louisville, 89 Ky., 112; Davidson v. Sterrett, 13 Ky. Law Rep., 176.

But after these suits were instituted the appellees, in the year 1890, procured an act of the Kentucky legislature, seeking to cure the defects in the assessment complained of, but this court has repeatedly held that no legislature can affect the rights of parties litigant enacted after the institution of the suits, therefore, the curative act of the legislature, attempting to affect the parties to these suits, must be treated as a nullity so far as it relates to the rights of appellants at the time of bringing their suits. (Allison v. Railway Co., 9 Bush, 247.)

But the appellees contend that the injunction ought not to have been granted because each of the appellants were charged with poll tax of $2 against appellant Nock and $6 against appellant Turner, and that the assessment of the poll tax was in form and valid.

We can not concur in this contention, although the assessment of poll tax against appellants may have been all right and legal, but still that would not authorize the sheriff to levy on appellant's land; for by the General Statutes, which was in force at the time, the sheriff had no right to levy on land and sell it for taxes until the personal property of the taxpayer had been exhausted.

The proof in these cases show clearly that appellants had an abundance of personal property within the corporate limits of the town to satisfy these taxes against them. (General Statutes, chapter 92.)

The judgment is, therefore, reversed and cause remanded, with directions that the court perpetuate the injunction in each of said cases and for further proceedings in accordance with this opinion.

The court delivered the following extension of opinion January 15, 1897:

Appellees having petitioned for an extension of the opinion heretofore filed in this case, and for further opinion, we hold that the levy or assessment of poll tax against the appellants was legal and valid, and the appellants are liable to the payment of the same, and as held in the opinion their lands were not liable to sale for the payment of the poll tax until their personal property was exhausted, and all that was intended in the former judgment was to perpetuate the injunction as to the collection of the ad valorem taxes levied, and the sale of their lands for the poll taxes, and the petition is overruled.

1989 Photos of the Truman Nock House from the Ashwood Avenue Historic District Nomination to the National Register of Historic Places

Related Links: